DOWNLOAD

12 min read • Marketing & sales

Getting ready for the energy consumer of the future

The energy sector is undergoing radical transformation as formerly passive consumers take control over their energy consumption and procurement. Based on the five stages of this transformation, we explain how it impacts the energy value chain and outline the capabilities that traditional providers must embrace if they are to meet the needs of the energy consumer of the future.

Today’s consumers expect convenience as a matter of course – and want greater control over everything they buy and do. This trend is now spreading from sectors such as retail and transport to energy, with customers moving from being passive consumers to playing a more active role in managing their energy consumption and procurement. And as digital technology, electric vehicles and distributed power generation all increase, these trends will accelerate and expand in scale. This will inevitably lead to a reorganized energy value chain and drive the emergence of new business models. What is the impact on incumbent energy providers in the oil, natural gas, power, and utility industries? Who will win the race to attract the energy consumer of the future? This article aims to map potential pathways and provides a framework to help business leaders develop the new essential capabilities.

Today’s consumers expect convenience as a matter of course – and want greater control over everything they buy and do. This trend is now spreading from sectors such as retail and transport to energy, with customers moving from being passive consumers to playing a more active role in managing their energy consumption and procurement. And as digital technology, electric vehicles and distributed power generation all increase, these trends will accelerate and expand in scale. This will inevitably lead to a reorganized energy value chain and drive the emergence of new business models. What is the impact on incumbent energy providers in the oil, natural gas, power, and utility industries? Who will win the race to attract the energy consumer of the future? This article aims to map potential pathways and provides a framework to help business leaders develop the new essential capabilities.

The evolving energy consumer

Within retail and transportation, consumers have already embraced the platform-based Amazon and Uber models, increasing their control and ensuring they get what they really need, when they need it, without the time and friction of going through intermediaries.

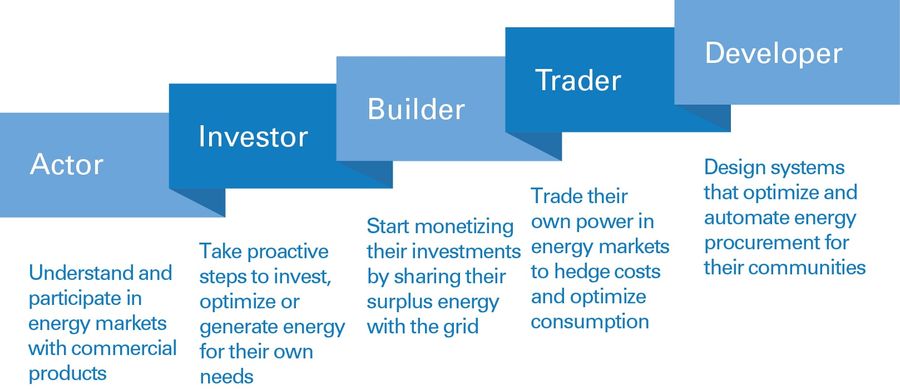

The same trends are moving into the energy world, where customers will increasingly adopt and adapt digital systems. These digital tools will enable customers to better meet their own needs, which will lead to new business models that will allow them to personalize their energy requirements. Based on our research and analysis, we see in Figure 1 a path that takes energy consumers globally through five main phases. Depending on local energy market development, some consumers in advanced countries are already ahead in this evolution.

Actors: Initially, consumers take advantage of energy efficiency and demand response programs in order to reduce their costs and carbon footprints. In certain US and European markets, they are aware of the unbundling of power generation and energy retail, which means they switch energy providers according to their preferences. They invest in smart devices that connect to their smart homes and cars to learn and understand their behaviors. They transact individually through digital channels with their energy providers, although they have limited ability to influence products and rates.

Investors: With increasingly energy-efficient and environmentally friendly behaviors, consumers put the focus on services that allow them to optimize their energy consumption. They install methods of distributed energy resources (such as photovoltaic solar panels on their rooftops and battery/energy storage on their side of the electric meter) and produce energy for self-consumption and for the grid. This is a fundamental change for utilities that means they have to rethink, and reverse, their unidirectional contracting strategies with their customers. As the gap in the total cost of mobility between electric and gasoline-powered vehicles narrows, consumers also assess which provides their best option for transport. This means traditional fuel retailers and suppliers need to transform their customer service as they start to compete with utilities. In advanced gas markets, consumers assess electric versus gas as an energy choice.

Builders: Consumers optimize their dependency on energy products. From a power perspective, customers make their spare supply available to their neighbors and transact with each other when needed, which offsets and reduces any reliance on grid services. This challenges the business models of incumbent utilities, which have traditionally invested in centralized, capital-intensive assets funded by utility customers. In terms of mobility, customers prefer not to spend time driving to, and waiting at, the gas station anymore, and this therefore threatens the relevance of this traditional value chain.

Traders: With the rise of battery systems and electric vehicles, consumers have turned into virtual traders. They start balancing – essentially hedging – their energy consumption with their own production. They tailor and schedule their activities to commercially advantageous times of the day and night. Even commercial and industrial consumers trade energy on digital platforms to the extent that they need to keep their core business operations running. Their energy consumption and generation systems are nimble and respond to surge pricing events, which further disintermediates incumbent power and fuel providers.

Developers: When these behaviors spread to entire communities, consumers work together to design energy systems that optimize resilience and cost for their own communities. In doing so, they build total systems that cover heating and cooling, building automation and smart neighborhoods, telecoms and broadband, and transportation and mobility. Utilities and oil and gas companies provide reliability and safety through their existing infrastructure, but they are no longer the sole providers of value-added services to consumers.

Preparing for the energy future

Building on the convergence of new technologies and business models, the energy consumers of the future are connected, commercial, and autonomous, virtually making (and transacting) power within an “Amazon of energy”. Consequently, they will play the leading role in the future world of energy – and incumbent players need to react now to be ready.

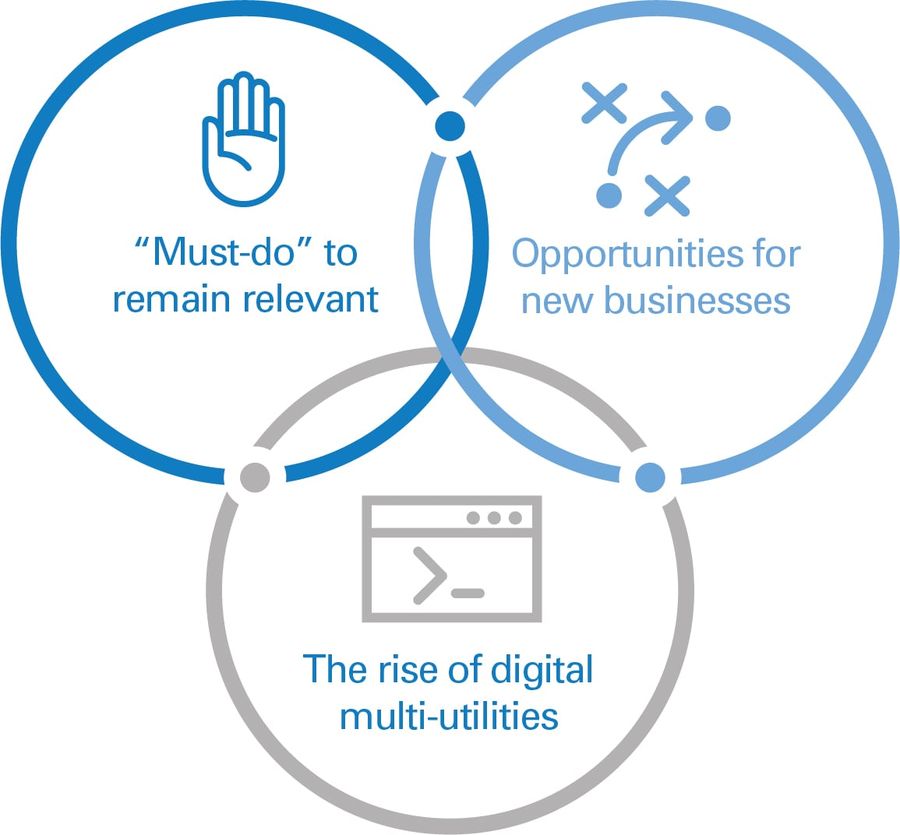

In order to adapt to how consumers use and produce energy, we see three ways in which businesses can respond, each of which will have radical impact on the energy value chain. These are shown in Figure 2. Equally, they will need to develop new capabilities to power this transformation, which we describe in the next section.

“Must-do” to remain relevant: Incumbent energy companies need to embrace the consumer-driven model and develop new digital businesses that offer convenience and new services around the delivery of their existing products to customers. They need to move from “sign in to your account” websites and “locate your nearest gas station” apps to interactive and personalized customer portals. Examples range from E.ON’s Energy Manager in Europe to Duke Energy’s Power Manager in the US and Diamond Energy’s bill reduction offer with Reposit Power in Australia. They need to focus on personalizing their products, including rethinking consumer-to-utility contracts, based on extensive investment in the customer experience and greater consumer understanding. Input from consumers further drives this personalization, which results in a new demand dynamic for energy generation and consumption.

Opportunities for new businesses: Companies may also venture out of their current business models and invest in developing new transformative products that respond to consumer desires for greater energy efficiency. Companies can incrementally extend their scope and reach to provide services further up and down the energy value chain. Some may engage in M&A transactions (for example, Swiss utility BKW acquiring 40-plus service businesses in engineering and building technology), while others will grow organically (for example, electric utility Southern Company offering fiber-optic solutions, as well as Shell venturing into mobile fueling services with TapUp). As a result, they augment their customer value propositions by pushing new products to their markets.

The rise of digital multi-utilities: New, disruptive intermediaries may become the ultimate digital multi- utilities, aggregating consumer needs, social preferences, energy availability, partner ecosystems, and delivery service optionality to fuel the consumer’s entire personalized energy lifestyle. As seen in other industries, such as media and travel, these businesses ingest and process massive amounts of data across various information sources and make consumer predictions based on artificial intelligence. In addition, the network platform effect allows consumers to monetize their assets across electricity, heating/cooling, and mobility fuels. By being independent from incumbents, this “energy-as- a-service” response provides the most personalization, convenience, and value-add, which we believe will offset the higher acquisition costs of implementing consumer digital technologies. This is also the most disruptive response for traditional energy providers, as it reduces the relevance of the historic energy value chain and forces oil and gas companies and electric utilities to collaborate (or compete) with each other.

There are already some good examples of how competitors in the industry are responding, as seen below.

How competitors are responding to the energy consumer of the future

Traditional energy companies

Large energy companies are already taking significant steps to shift their focus, as previously discussed in “Shaping the oil company of the future” in Prism issue 1, 2019. Many existing utilities struggle with lack of direct engagement with local consumers, although some are aiming to bridge this gap. For example, EDF Luminus offers flexibility, energy assets (solar panels, battery packs, electric vehicle chargers), and services beyond traditional gas and electricity. Overall, major oil and gas operators invested $3–4 billion in low-carbon energy solutions in 2018 – slightly over 1 percent of their capital budgets. Given that 2018 global investments in distributed energy and clean technology overall totaled more than $300 billion, oil and gas companies are not the only players.

Consumer products companies

On the consumer products side, smart home vendors are helping customers control the temperature in their houses, reduce their energy usage, and make significant savings on their bills. There is a fierce battle raging for control of the smart home between market leader Google Nest, followed by Ecobee, Honeywell, Samsung, and Amazon’s Alexa platform. All are investing massively in order to own the new smart home, managed via apps and voice control. This is just the beginning – companies such as Ecobee are leveraging artificial intelligence to listen, learn, and respond to consumer behavior and market pricing, automatically adjusting energy consumption based on real-time weather and electricity rates and acting as virtual batteries for energy. In the mobility space, companies are starting to penetrate the consumer energy market with offerings that directly affect energy consumption – for example, Volkswagen’s Elli, a webshop for green power supply and charging solutions for electric vehicles.

New energy companies

New entrants are seizing specific opportunities, based on in-depth knowledge of generation and consumption patterns. Companies such as LO3 Energy and GridPlus in the US, Power Ledger and GreenSync in Australia/the UK, and Vandebron and Powerpeers in the Netherlands are beginning to reshape how energy is distributed across the grid by allowing consumers to transact energy with one another. In Germany, digital platforms for B2B power and gas procurement are emerging. Players such as enPortal, e.less, enermarket, and Verivox for retail, as well as tender365 and enmacc for wholesale, support fully digitalized, end-to-end buying and selling energy capabilities. While they connect buyers with utilities today, they will become pure P2P trading businesses in the next five years. On the gasoline side, start- ups such as filld.com and startyoshi.com began by providing delivery to individual cars, and are now expanding to bundle maintenance services and offer discounts on retail gasoline.

The spark for action

As energy consumers favor and adopt offerings from integrated, digital multi-utility and energy-as-a-service business models, the global energy value chain is finding itself on the cusp of being fundamentally disrupted. Traditional gas and electric utilities, as well as liquid-fuel providers, certainly have a valuable set of competitive advantages across customers, products, and logistics, but these are being challenged by new entrants.

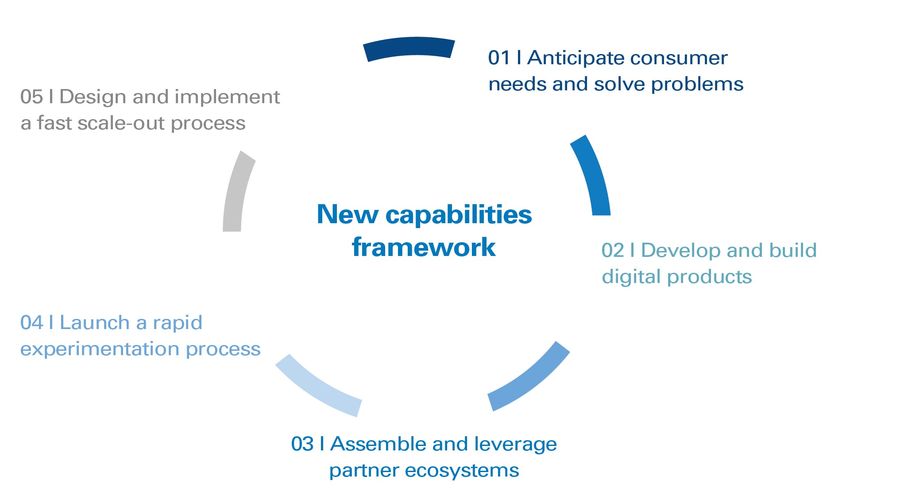

We believe the businesses that are able to listen to their customers’ behaviors across multiple platforms and rapidly offer them tailored energy solutions will be successful in the long term. Incumbent energy providers therefore need to take steps to build new communication channels, foundational product capabilities, and the advanced analytics necessary to remain the suppliers of choice. We show five key capabilities that are fundamental to achieving the necessary transformation in Figure 3. Many of these are new to established companies’ mind-sets:

01| Anticipate consumer needs and solve problems: Based on specific local market conditions, energy companies need to leverage issue-centric problem solving to avoid implementing today’s “best” practices, and instead craft their consumers’ “next” practices. Previously, energy providers followed best practices to solve relatively predictable consumer problems that were flagged to them. In the more fluid future market, they will need to move to convergence- driven problem solving. They need to anticipate new, future needs and actually identify solutions to problems before consumers realize there is an issue. This can only be achieved by adopting consumer anticipation-based design thinking and aggressively expanding direct consumer engagement, so they can understand and incorporate consumer insight into design and innovation processes.

02| Develop and build digital products: Players need to invest boldly in the resources and skills which allow their teams to develop and fine-tune their digital technologies and offerings. The objective should be to align energy product offerings with energy customer priorities as they evolve. Technologies that capture energy customer behaviors and patterns spanning multiple information channels will be the most relevant investments for energy providers to personalize their solutions. The capabilities to strategically design, engineer, and architect digital businesses will be key to unlocking digital opportunities.

03| Assemble and leverage ecosystems of partners: Business leaders need to actively develop and maintain networks of partners that bring unique and complementary capabilities to their organizations. Energy-as-a-service means that customers play the central role in the transformation of the industry value chain. Traditional power utilities, oil and gas producers and retailers, technology developers, and start-ups, among others, should be able to leverage synergies to satisfy energy customer expectations. Beyond traditional supplier partnerships, companies also need to manage technology ventures that can be monitored, evaluated, and scaled up once de-risked, as well as corporate-start-up collaboration platforms such as accelerators and incubators, to bring in new, breakthrough thinking.

04| Launch a rapid experimentation process: To compete in the fast-paced digital environment, leaders need to implement comprehensive processes that let their organizations iterate to tangibly measure – and learn – from testing and experimenting with new products and business models before engaging in pilots and commercialization at scale. Managing technology pilots requires rigor and discipline – and a broad view of the business. So the company needs a structure to enable teams to ideate, a process to guide the incubation stage, and a system to link the learnings back to the overall business.

05| Design and implement a fast scale-out process: Energy companies have been traditionally strong at managing projects, infrastructure, and commodities through multi-year and decade-long cycles. For the future energy consumer, they will need to transform their established value propositions and at a much faster pace. Their capabilities to scale out solutions to their markets will become critical. The key strength and competitive advantage will therefore rely on a nimble, yet effective, commercialization process and go-to-market approach, which will require an agile mind-set for change and collaboration across multiple corporate functions.

Equipped with this capabilities framework, business leaders can start setting the new direction for their companies in line with the requirements of future energy consumers, and therefore take leading roles in the future ecosystem and value chain.

Insight for the executive

The energy consumer of the future will adopt and adapt digital systems that will enable them to control their energy footprints, which will lead to new business models of energy- as-a-service. Energy companies will face multiple disruptions to their businesses, and need to act in new and different ways to remain ahead:

- Develop new digital businesses that offer convenience and personalized options for delivery of their existing energy products to customers.

- Launch new energy products to respond to particular customer desires, strengthening their offerings as broader energy service providers.

- Transform their businesses towards digital multi-utilities that can offer integrated and optimized total energy solutions to their customers.

The energy transition is also opening the door to new players such as smart device manufacturers and network developers, which are focusing on interacting with customers and understanding their needs to provide personalized solutions. These new ecosystems represent not only challenges, but also opportunities, for incumbent energy companies. Ultimately, incumbents need to shift their core engineering capabilities from infrastructure assets to software platforms and digital assets. Such a transformation requires significant effort to develop new capabilities:

- Anticipating consumer needs and solving problems

- Developing and building digital products

- Assembling and leveraging ecosystems of partners

- Launching a rapid experimentation process

- Designing and implementing a fast scale-out process

The energy sector is undergoing radical transformation as formerly passive consumers take control over their energy consumption and procurement. Based on the five stages of this transformation, we explain how it impacts the energy value chain and outline the capabilities that traditional providers must embrace if they are to meet the needs of the energy consumer of the future.

Today’s consumers expect convenience as a matter of course – and want greater control over everything they buy and do. This trend is now spreading from sectors such as retail and transport to energy, with customers moving from being passive consumers to playing a more active role in managing their energy consumption and procurement. And as digital technology, electric vehicles and distributed power generation all increase, these trends will accelerate and expand in scale. This will inevitably lead to a reorganized energy value chain and drive the emergence of new business models. What is the impact on incumbent energy providers in the oil, natural gas, power, and utility industries? Who will win the race to attract the energy consumer of the future? This article aims to map potential pathways and provides a framework to help business leaders develop the new essential capabilities.

The evolving energy consumer

Within retail and transportation, consumers have already embraced the platform-based Amazon and Uber models, increasing their control and ensuring they get what they really need, when they need it, without the time and friction of going through intermediaries.

The same trends are moving into the energy world, where customers will increasingly adopt and adapt digital systems. These digital tools will enable customers to better meet their own needs, which will lead to new business models that will allow them to personalize their energy requirements. Based on our research and analysis, we see in Figure 1 a path that takes energy consumers globally through five main phases. Depending on local energy market development, some consumers in advanced countries are already ahead in this evolution.

Actors: Initially, consumers take advantage of energy efficiency and demand response programs in order to reduce their costs and carbon footprints. In certain US and European markets, they are aware of the unbundling of power generation and energy retail, which means they switch energy providers according to their preferences. They invest in smart devices that connect to their smart homes and cars to learn and understand their behaviors. They transact individually through digital channels with their energy providers, although they have limited ability to influence products and rates.

Investors: With increasingly energy-efficient and environmentally friendly behaviors, consumers put the focus on services that allow them to optimize their energy consumption. They install methods of distributed energy resources (such as photovoltaic solar panels on their rooftops and battery/energy storage on their side of the electric meter) and produce energy for self-consumption and for the grid. This is a fundamental change for utilities that means they have to rethink, and reverse, their unidirectional contracting strategies with their customers. As the gap in the total cost of mobility between electric and gasoline-powered vehicles narrows, consumers also assess which provides their best option for transport. This means traditional fuel retailers and suppliers need to transform their customer service as they start to compete with utilities. In advanced gas markets, consumers assess electric versus gas as an energy choice.

Builders: Consumers optimize their dependency on energy products. From a power perspective, customers make their spare supply available to their neighbors and transact with each other when needed, which offsets and reduces any reliance on grid services. This challenges the business models of incumbent utilities, which have traditionally invested in centralized, capital-intensive assets funded by utility customers. In terms of mobility, customers prefer not to spend time driving to, and waiting at, the gas station anymore, and this therefore threatens the relevance of this traditional value chain.

Traders: With the rise of battery systems and electric vehicles, consumers have turned into virtual traders. They start balancing – essentially hedging – their energy consumption with their own production. They tailor and schedule their activities to commercially advantageous times of the day and night. Even commercial and industrial consumers trade energy on digital platforms to the extent that they need to keep their core business operations running. Their energy consumption and generation systems are nimble and respond to surge pricing events, which further disintermediates incumbent power and fuel providers.

Developers: When these behaviors spread to entire communities, consumers work together to design energy systems that optimize resilience and cost for their own communities. In doing so, they build total systems that cover heating and cooling, building automation and smart neighborhoods, telecoms and broadband, and transportation and mobility. Utilities and oil and gas companies provide reliability and safety through their existing infrastructure, but they are no longer the sole providers of value-added services to consumers.

Preparing for the energy future

Building on the convergence of new technologies and business models, the energy consumers of the future are connected, commercial, and autonomous, virtually making (and transacting) power within an “Amazon of energy”. Consequently, they will play the leading role in the future world of energy – and incumbent players need to react now to be ready.

In order to adapt to how consumers use and produce energy, we see three ways in which businesses can respond, each of which will have radical impact on the energy value chain. These are shown in Figure 2. Equally, they will need to develop new capabilities to power this transformation, which we describe in the next section.

“Must-do” to remain relevant: Incumbent energy companies need to embrace the consumer-driven model and develop new digital businesses that offer convenience and new services around the delivery of their existing products to customers. They need to move from “sign in to your account” websites and “locate your nearest gas station” apps to interactive and personalized customer portals. Examples range from E.ON’s Energy Manager in Europe to Duke Energy’s Power Manager in the US and Diamond Energy’s bill reduction offer with Reposit Power in Australia. They need to focus on personalizing their products, including rethinking consumer-to-utility contracts, based on extensive investment in the customer experience and greater consumer understanding. Input from consumers further drives this personalization, which results in a new demand dynamic for energy generation and consumption.

Opportunities for new businesses: Companies may also venture out of their current business models and invest in developing new transformative products that respond to consumer desires for greater energy efficiency. Companies can incrementally extend their scope and reach to provide services further up and down the energy value chain. Some may engage in M&A transactions (for example, Swiss utility BKW acquiring 40-plus service businesses in engineering and building technology), while others will grow organically (for example, electric utility Southern Company offering fiber-optic solutions, as well as Shell venturing into mobile fueling services with TapUp). As a result, they augment their customer value propositions by pushing new products to their markets.

The rise of digital multi-utilities: New, disruptive intermediaries may become the ultimate digital multi- utilities, aggregating consumer needs, social preferences, energy availability, partner ecosystems, and delivery service optionality to fuel the consumer’s entire personalized energy lifestyle. As seen in other industries, such as media and travel, these businesses ingest and process massive amounts of data across various information sources and make consumer predictions based on artificial intelligence. In addition, the network platform effect allows consumers to monetize their assets across electricity, heating/cooling, and mobility fuels. By being independent from incumbents, this “energy-as- a-service” response provides the most personalization, convenience, and value-add, which we believe will offset the higher acquisition costs of implementing consumer digital technologies. This is also the most disruptive response for traditional energy providers, as it reduces the relevance of the historic energy value chain and forces oil and gas companies and electric utilities to collaborate (or compete) with each other.

There are already some good examples of how competitors in the industry are responding, as seen below.

How competitors are responding to the energy consumer of the future

Traditional energy companies

Large energy companies are already taking significant steps to shift their focus, as previously discussed in “Shaping the oil company of the future” in Prism issue 1, 2019. Many existing utilities struggle with lack of direct engagement with local consumers, although some are aiming to bridge this gap. For example, EDF Luminus offers flexibility, energy assets (solar panels, battery packs, electric vehicle chargers), and services beyond traditional gas and electricity. Overall, major oil and gas operators invested $3–4 billion in low-carbon energy solutions in 2018 – slightly over 1 percent of their capital budgets. Given that 2018 global investments in distributed energy and clean technology overall totaled more than $300 billion, oil and gas companies are not the only players.

Consumer products companies

On the consumer products side, smart home vendors are helping customers control the temperature in their houses, reduce their energy usage, and make significant savings on their bills. There is a fierce battle raging for control of the smart home between market leader Google Nest, followed by Ecobee, Honeywell, Samsung, and Amazon’s Alexa platform. All are investing massively in order to own the new smart home, managed via apps and voice control. This is just the beginning – companies such as Ecobee are leveraging artificial intelligence to listen, learn, and respond to consumer behavior and market pricing, automatically adjusting energy consumption based on real-time weather and electricity rates and acting as virtual batteries for energy. In the mobility space, companies are starting to penetrate the consumer energy market with offerings that directly affect energy consumption – for example, Volkswagen’s Elli, a webshop for green power supply and charging solutions for electric vehicles.

New energy companies

New entrants are seizing specific opportunities, based on in-depth knowledge of generation and consumption patterns. Companies such as LO3 Energy and GridPlus in the US, Power Ledger and GreenSync in Australia/the UK, and Vandebron and Powerpeers in the Netherlands are beginning to reshape how energy is distributed across the grid by allowing consumers to transact energy with one another. In Germany, digital platforms for B2B power and gas procurement are emerging. Players such as enPortal, e.less, enermarket, and Verivox for retail, as well as tender365 and enmacc for wholesale, support fully digitalized, end-to-end buying and selling energy capabilities. While they connect buyers with utilities today, they will become pure P2P trading businesses in the next five years. On the gasoline side, start- ups such as filld.com and startyoshi.com began by providing delivery to individual cars, and are now expanding to bundle maintenance services and offer discounts on retail gasoline.

The spark for action

As energy consumers favor and adopt offerings from integrated, digital multi-utility and energy-as-a-service business models, the global energy value chain is finding itself on the cusp of being fundamentally disrupted. Traditional gas and electric utilities, as well as liquid-fuel providers, certainly have a valuable set of competitive advantages across customers, products, and logistics, but these are being challenged by new entrants.

We believe the businesses that are able to listen to their customers’ behaviors across multiple platforms and rapidly offer them tailored energy solutions will be successful in the long term. Incumbent energy providers therefore need to take steps to build new communication channels, foundational product capabilities, and the advanced analytics necessary to remain the suppliers of choice. We show five key capabilities that are fundamental to achieving the necessary transformation in Figure 3. Many of these are new to established companies’ mind-sets:

01| Anticipate consumer needs and solve problems: Based on specific local market conditions, energy companies need to leverage issue-centric problem solving to avoid implementing today’s “best” practices, and instead craft their consumers’ “next” practices. Previously, energy providers followed best practices to solve relatively predictable consumer problems that were flagged to them. In the more fluid future market, they will need to move to convergence- driven problem solving. They need to anticipate new, future needs and actually identify solutions to problems before consumers realize there is an issue. This can only be achieved by adopting consumer anticipation-based design thinking and aggressively expanding direct consumer engagement, so they can understand and incorporate consumer insight into design and innovation processes.

02| Develop and build digital products: Players need to invest boldly in the resources and skills which allow their teams to develop and fine-tune their digital technologies and offerings. The objective should be to align energy product offerings with energy customer priorities as they evolve. Technologies that capture energy customer behaviors and patterns spanning multiple information channels will be the most relevant investments for energy providers to personalize their solutions. The capabilities to strategically design, engineer, and architect digital businesses will be key to unlocking digital opportunities.

03| Assemble and leverage ecosystems of partners: Business leaders need to actively develop and maintain networks of partners that bring unique and complementary capabilities to their organizations. Energy-as-a-service means that customers play the central role in the transformation of the industry value chain. Traditional power utilities, oil and gas producers and retailers, technology developers, and start-ups, among others, should be able to leverage synergies to satisfy energy customer expectations. Beyond traditional supplier partnerships, companies also need to manage technology ventures that can be monitored, evaluated, and scaled up once de-risked, as well as corporate-start-up collaboration platforms such as accelerators and incubators, to bring in new, breakthrough thinking.

04| Launch a rapid experimentation process: To compete in the fast-paced digital environment, leaders need to implement comprehensive processes that let their organizations iterate to tangibly measure – and learn – from testing and experimenting with new products and business models before engaging in pilots and commercialization at scale. Managing technology pilots requires rigor and discipline – and a broad view of the business. So the company needs a structure to enable teams to ideate, a process to guide the incubation stage, and a system to link the learnings back to the overall business.

05| Design and implement a fast scale-out process: Energy companies have been traditionally strong at managing projects, infrastructure, and commodities through multi-year and decade-long cycles. For the future energy consumer, they will need to transform their established value propositions and at a much faster pace. Their capabilities to scale out solutions to their markets will become critical. The key strength and competitive advantage will therefore rely on a nimble, yet effective, commercialization process and go-to-market approach, which will require an agile mind-set for change and collaboration across multiple corporate functions.

Equipped with this capabilities framework, business leaders can start setting the new direction for their companies in line with the requirements of future energy consumers, and therefore take leading roles in the future ecosystem and value chain.

Insight for the executive

The energy consumer of the future will adopt and adapt digital systems that will enable them to control their energy footprints, which will lead to new business models of energy- as-a-service. Energy companies will face multiple disruptions to their businesses, and need to act in new and different ways to remain ahead:

- Develop new digital businesses that offer convenience and personalized options for delivery of their existing energy products to customers.

- Launch new energy products to respond to particular customer desires, strengthening their offerings as broader energy service providers.

- Transform their businesses towards digital multi-utilities that can offer integrated and optimized total energy solutions to their customers.

The energy transition is also opening the door to new players such as smart device manufacturers and network developers, which are focusing on interacting with customers and understanding their needs to provide personalized solutions. These new ecosystems represent not only challenges, but also opportunities, for incumbent energy companies. Ultimately, incumbents need to shift their core engineering capabilities from infrastructure assets to software platforms and digital assets. Such a transformation requires significant effort to develop new capabilities:

- Anticipating consumer needs and solving problems

- Developing and building digital products

- Assembling and leveraging ecosystems of partners

- Launching a rapid experimentation process

- Designing and implementing a fast scale-out process

RELATED INFORMATION

A Conversation Profits with Principles – The Transformation of Royal Dutch/Shell

With more than 100,000 employees and assets valued at $80 billion, the Royal Dutch/Shell Group is a global giant in the energy industry, involved in the whole production process of fossil fuels – –…

IT Rightsizing

The credit crisis, increasing energy prices and overheated stock markets are all indicators of a possible economic downturn. Like all budgets, IT budgets will be cut. IT "rightsizing" is a balanced…

Advanced Metering Management

Environmental and economic pressures have seen many utilities reconsidering the use of smart metering technology to end the high operational costs associated with traditional energy usage monitoring…